Was this worth a coffee? Not a flat white. Just a regular, sensible £2 coffee. If this helped, feel free to buy me one. If it didn't, keep your money — that's only fair.

Centralised Retirement Proposition (CRP®)

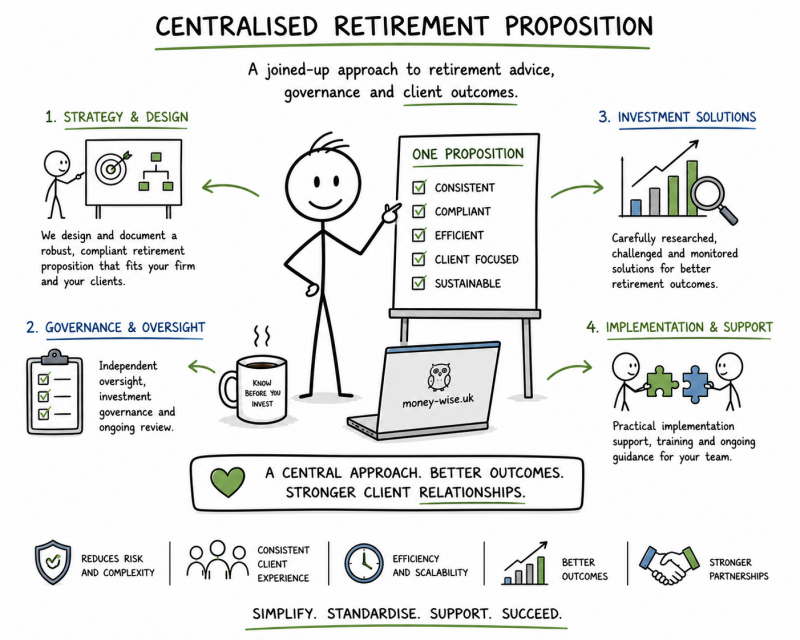

A Governance Framework for Retirement Income Advice

What Is a Centralised Retirement Proposition?

A Centralised Retirement Proposition (CRP®) is a structured governance framework designed to help financial planning firms deliver consistent, sustainable and regulator-ready retirement income advice.

While many firms operate a Centralised Investment Proposition (CIP), fewer have developed a documented and repeatable retirement income governance framework.

The CRP® bridges that gap.

Developed by Money Wise UK®, the CRP® provides a structured approach to:

- Pension drawdown processes

- Sustainable withdrawal strategies

- Retirement income reviews

- Sequencing risk management

- Consumer Duty alignment

- Ongoing suitability governance

The term Centralised Retirement Proposition (CRP®) is a registered trademark of Money Wise UK®.

Why Retirement Governance Matters Now

The UK retirement landscape has changed significantly.

-

Over 12 million people in the UK are aged 65+ (ONS data).

-

Flexible pension drawdown has become the dominant retirement income strategy since Pension Freedoms (2015).

-

Retirements often span 25–30 years.

-

The FCA’s Retirement Income Advice Thematic Review (TR24/1) has increased scrutiny on sustainable withdrawal planning.

At the same time, the introduction of Consumer Duty requires firms to evidence good outcomes, not simply suitable recommendations.

Retirement advice now requires:

-

Structured income planning

-

Clear documentation

-

Ongoing sustainability monitoring

-

Defined review processes

Without a documented retirement income framework, firms may face:

-

Inconsistent adviser approaches

-

Increased compliance exposure

-

Key-person dependency

-

Consumer Duty vulnerability

Introducing the CRP® Framework

The Centralised Retirement Proposition (CRP®) is a repeatable governance structure for retirement advice.

It is not a model portfolio service.

It is not a retirement product.

It is a documented retirement income governance framework.

What the CRP® Includes

The CRP® framework provides:

-

A clearly defined retirement client journey

-

A structured pension drawdown process

-

Documented withdrawal strategy governance

-

Sequencing risk communication guidance

-

Standardised retirement review templates

-

Consumer Duty-aligned documentation support

-

Behavioural guidance around income volatility

This enables firms to centralise retirement advice in the same way many have centralised investment management.

Supporting FCA Expectations

The CRP® framework aligns with:

-

FCA Retirement Income Advice Thematic Review (TR24/1)

-

Consumer Duty requirements

-

Ongoing suitability obligations

-

Sustainability stress-testing expectations

It helps firms evidence:

-

Sustainable withdrawal methodology

-

Structured retirement reviews

-

Clear communication of income risks

-

Governance oversight of decumulation advice

Who Is the CRP® Designed For?

The CRP® is designed for:

-

Independent financial advisers (IFAs)

-

Chartered financial planning firms

-

Retirement specialists

-

Firms with growing retired client bases

-

Advice businesses seeking stronger governance documentation

It is particularly relevant for firms where:

-

More than 50% of AUM is in decumulation

-

Advisers use flexible drawdown

-

Retirement income reviews are increasing

-

Consumer Duty governance is under review

Distribution and Licensing

Money Wise UK® owns the CRP® intellectual property.

Newbury Street Research holds a distribution licence and supports:

-

Implementation discussions

-

Onboarding

-

Customisation coordination

-

Ongoing relationship management

Fee Structure

The CRP® is positioned as a governance infrastructure solution.

Template Plus Licence

£2,500 + VAT

Includes:

-

Core CRP® documentation

-

Light firm-level customisation

-

Implementation guidance

Estimated delivery time: approximately two working days.

Additional support available at £400 per day.

Optional Annual Licence

£1,000 per annum

Provides:

-

Regulatory updates

-

Template enhancements

-

Framework refinements

-

Continued brand association

Bespoke Retirement Integration

For firms requiring deeper retirement income restructuring, further support may be available via:

Retirement Advice Requires Structured Governance

As:

-

Retirements extend,

-

Pension drawdown grows,

-

Regulatory scrutiny increases,

firms require more than retirement products.

They require retirement governance.

The Centralised Retirement Proposition (CRP®) provides that structure.

Was this worth a coffee? Not a flat white. Just a regular, sensible £2 coffee. If this helped, feel free to buy me one. If it didn't, keep your money — that's only fair.

CRP, Centralised Retirement Propostion: Retirement Planning Simplified ® is a registered trademark. This means that both the words and the logo are protected and cannot be reproduced without express permission.