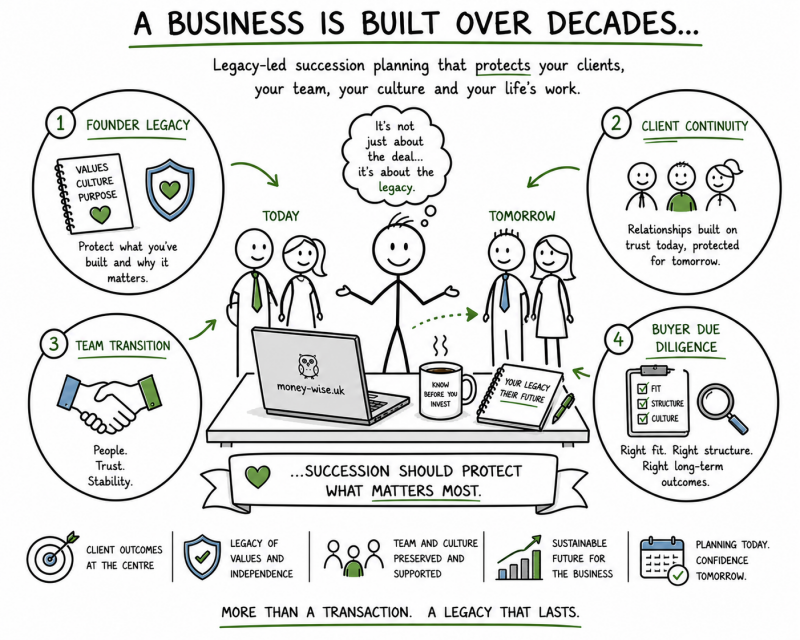

Selling Your Financial Planning Business: A Legacy-Led Approach for UK Advisers

A Different Conversation About Selling an IFA Business

I previously worked in a business where the owner and shareholder chose to sell to a large consolidator.

That experience shaped my thinking.

Selling a financial planning business is rarely just a transaction. In practice, advisers tend to fall into two broad camps:

-

Those primarily focused on achieving the highest possible price, with less emphasis on long-term outcomes for clients or staff

-

Those who care deeply about legacy—how clients are treated, how staff are supported, and what happens after they step away

My focus is firmly on the second group.

This page is written for advisers who want to exit well, not just exit quickly.

Why the FCA Is Paying Closer Attention to Business Sales

Recent regulatory scrutiny has reinforced something many advisers already know: how a business is sold matters.

The Financial Conduct Authority has increasingly focused on:

-

Consumer Duty outcomes during ownership change

-

Continuity of advice and service following acquisitions

-

The risk of clients becoming “orphaned” or moved into unsuitable propositions

-

The sustainability of charging structures post-sale

-

Governance, oversight, and evidencing decision-making

In simple terms, a sale that looks good on paper but results in poorer client outcomes is increasingly hard to defend.

A well-prepared, well-documented business—aligned with Consumer Duty principles—is not just more compliant; it is more attractive to the right buyer.

Step One: Truly Understanding Your Business

This may sound obvious, but it is often underestimated.

In hindsight, one of the strengths of the business I worked in was that we understood every moving part, including where the risks sat.

A buyer, and a regulator, will expect clarity across several dimensions.

1. Your Clients and Assets

Beyond headline AUM, you should clearly understand:

-

Where assets are held (platforms, wrappers, products)

-

Client age profiles and how assets are distributed across generations

-

Concentration risk (key clients, family groups, employer schemes)

-

Evidence of engagement with next-generation clients

This is not just valuation data—it is outcome risk analysis.

2. Your Advice and Service Processes

Increasingly, buyers want to know whether the business can operate without you.

That means having clear evidence of:

-

Documented advice processes

-

Client meeting records and review histories

-

File review outcomes and remediation logs

-

Complaints registers (even if nil)

-

Audit trails and governance reviews

-

Consumer Duty assessments and outcomes monitoring

A simple test I often use:

Could someone understand and run this business without speaking to you?

If the answer is yes, you are on the right track.

Reducing Risk Increases Value

One of the most powerful (and overlooked) benefits of good governance is risk reduction.

Once you start formally recording:

-

Known risks

-

Mitigating actions

-

Oversight and review cycles

Your actual business risk falls significantly.

This is good practice whether you sell or not—but it becomes critical when preparing for due diligence.

Understanding What Your Business Really Offers

Financial planning is deeply personal.

Two firms with identical AUM can be completely different businesses.

You should be able to clearly articulate:

-

Who you serve best

-

What makes your approach distinctive

-

Why clients stay with you

-

How advice is delivered, not just what products are used

Key questions buyers will ask include:

-

Can the business operate without the founder?

-

Is revenue recurring and sustainable?

-

Is the charging structure fair and defendable under Consumer Duty?

-

Does the proposition align with how clients actually use the service?

Clarity here doesn’t reduce value, it protects it.

Personal Objectives: Price vs Legacy

For some advisers, the primary goal is achieving the highest possible sale price.

That is a valid choice, but it leads to very different outcomes.

If you are thinking more holistically, your questions may include:

-

How will my clients be treated after I step away?

-

Will they receive a similar planning-led service?

-

What happens to my team?

-

Can staff be retained and developed within the acquiring firm?

-

Do I want a clean exit, or a phased transition?

For many advisers, retirement is not a single event but a gradual transition—introducing new advisers, supporting clients through change, and stepping back with confidence.

This approach often results in better outcomes for everyone, even if the headline price is not the only measure of success.

A Growing List of Like-Minded Firms

Over time, I intend to build a curated list of smaller, values-aligned acquirers—firms that are growing thoughtfully rather than simply consolidating for scale.

These are businesses that:

-

Prioritise client outcomes

-

Respect existing planning cultures

-

Value staff continuity

-

Understand the responsibility that comes with taking over client relationships

Alongside this, I will share links to practical resources that help advisers prepare—whether a sale is imminent or several years away.

Final Thought

Selling your business is not just a commercial decision.

It is the final chapter of your professional life’s work.

Handled well, it can secure your retirement, protect your clients, and preserve the culture you spent decades building.

That, to me, is a legacy worth planning for.

Frequently Asked Questions: Selling a Financial Planning Business in the UK

When is the right time to sell an IFA or financial planning business?

There is rarely a single “right” time, but the best outcomes tend to come when advisers plan several years in advance.

Preparing early allows you to:

-

Strengthen governance and documentation

-

Reduce business and regulatory risk

-

Introduce succession or phased transition options

-

Protect client outcomes and staff continuity

Even if a sale is not imminent, getting the business into a sale-ready position is simply good business practice.

What does the FCA expect when a financial planning business is sold?

The Financial Conduct Authority does not approve or block business sales, but it does expect firms to demonstrate that:

-

Client outcomes are protected before, during, and after the transaction

-

Advice continuity and service standards are maintained

-

Charging structures remain fair and defensible

-

Governance, oversight, and record-keeping are robust

Under Consumer Duty, firms must be able to evidence that a sale does not lead to foreseeable harm to clients.

Does Consumer Duty apply when selling a business?

Yes.

Consumer Duty does not stop at the point of sale. Both the selling firm and the acquiring firm need to consider:

-

Whether clients are likely to receive the same or better outcomes

-

Whether services and costs remain appropriate

-

How vulnerable or less engaged clients are supported during transition

A lack of planning around this has been highlighted in recent FCA supervisory work.

What makes an IFA business more attractive to the right buyer?

Beyond assets under management, buyers increasingly focus on:

-

Clear and repeatable advice processes

-

Strong client records and review histories

-

Evidence of governance, audits, and file reviews

-

Sustainable and transparent charging structures

-

A business that can operate without over-reliance on the founder

Reducing key-person risk often improves both value and buyer quality.

Is the highest sale price always the best outcome?

Not necessarily.

For some advisers, price is the primary driver. For others, legacy matters more.

A legacy-led sale may prioritise:

-

Client service continuity

-

Cultural alignment

-

Staff retention and development

-

A phased or supported transition

These factors do not always reduce value—but they do influence who the right buyer is.

What happens to my clients after I sell?

That depends entirely on who you sell to and how the transition is managed.

Key considerations include:

-

Whether clients remain within a planning-led proposition

-

Whether adviser relationships are preserved or changed

-

How communication and consent are handled

-

Whether vulnerable or elderly clients receive additional support

Increasingly, the FCA expects firms to be able to evidence how these risks were considered and mitigated.

What about my staff—are they usually retained?

Staff outcomes vary widely.

Some acquisitions are designed around long-term integration and growth, while others focus primarily on asset transfer.

If staff continuity matters to you, this should be:

-

Explicitly discussed early in the process

-

Reflected in buyer selection, not just price

-

Supported by clear role definitions and future pathways

A well-run business with documented processes is often easier for staff to transition into.

Can I sell my business and still remain involved?

Yes. Many advisers choose a phased exit, which may involve:

-

Gradually reducing client responsibility

-

Supporting the handover of relationships

-

Remaining involved in mentoring or oversight

-

Aligning retirement timing with client transitions

This approach can reduce risk for clients, staff, and the acquiring firm.

Do I need everything to be “perfect” before selling?

No—but clarity matters.

Buyers and regulators are generally more comfortable with:

-

Known risks that are documented and understood

-

Evidence of ongoing improvement

-

Honest disclosure rather than hidden issues

Trying to present a flawless business often creates more problems than it solves.

Where can I find firms that share a similar ethos?

Over time, this page will include:

-

A curated list of smaller, values-aligned acquirers

-

Links to specialist resources around succession and governance

-

Practical tools to help advisers prepare at their own pace

The aim is to support informed decisions—not to push a particular outcome.

Was this worth a coffee? Not a flat white. Just a regular, sensible £2 coffee. If this helped, feel free to buy me one. If it didn't, keep your money — that's only fair.