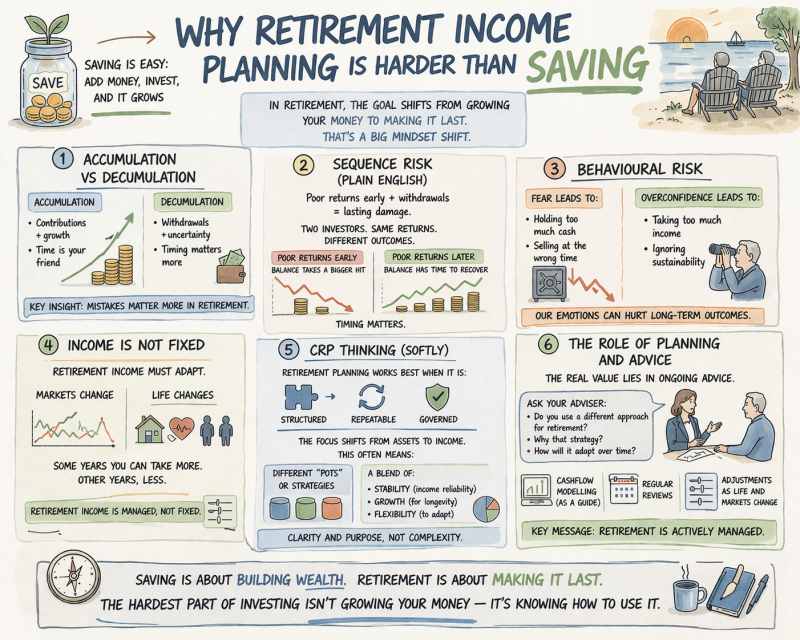

Saving, in many ways, is the easier part of investing.

You add money.

You invest it.

Over time, it grows.

Retirement is different.

This is where many people struggle — and, if we are honest, many advisers are still learning to think differently too.

Because the focus shifts.

It is no longer about growing your money.

It is about making it last.

That is a significant change in mindset.

Accumulation vs Decumulation

During your working life, you are in the accumulation phase.

- You contribute regularly

- Your investments grow over time

- Time is your biggest ally

Market falls matter less because you are still adding money.

Retirement flips this completely.

You move into decumulation:

- You are withdrawing money

- Markets still move unpredictably

- Timing becomes far more important

Key insight: Mistakes matter more in retirement.

A poor decision early on can have a lasting impact, because you are no longer adding to the pot — you are drawing from it.

Sequence Risk (In Plain English)

One of the biggest risks in retirement is something called sequence risk.

In simple terms:

If markets fall early in retirement while you are taking income, it can cause lasting damage.

Imagine two investors:

- Both achieve the same average return over time

- But one experiences poor returns early, the other later

The outcomes can be very different.

Why?

Because withdrawals during a downturn reduce the amount left invested — meaning less opportunity to recover when markets improve.

No complex maths needed.

Just timing.

Behavioural Risk

Alongside market risk sits something equally important: behavioural risk.

This is how we react.

Fear can lead to:

- Holding too much in cash

- Selling investments at the worst possible time

Overconfidence can lead to:

- Taking too much income too soon

- Ignoring whether income is sustainable

Both can damage long-term outcomes.

Retirement planning is as much about managing behaviour as it is about managing investments.

Income Is Not Fixed

One of the biggest misconceptions is that retirement income should behave like a salary.

It doesn’t.

Retirement income needs to adapt because:

- Markets change

- Inflation changes

- Life changes

Some years may allow for higher withdrawals. Others may require restraint.

Retirement income is not fixed — it is managed.

A Different Way of Thinking (CRP Thinking)

When I started developing a structured retirement process nearly two years ago, one thing became clear — particularly when reflecting on the direction from the Financial Conduct Authority.

Retirement planning works best when it is:

- Structured

- Repeatable

- Governed

One of the key shifts is recognising that accumulation strategies do not always translate directly into retirement.

The focus changes from assets to income.

This often leads to a more thoughtful structure, such as:

- Different “pots” or strategies

- A blend of:

- Stability (for income reliability)

- Growth (to support longevity)

- Flexibility (to adapt over time)

This isn’t about complexity.

It’s about clarity and purpose.

The Role of Planning and Advice

In my experience, the real value lies in ongoing advice.

If you are speaking to a financial adviser, it is worth asking:

- Do you have a different approach for retirement compared to accumulation?

- Why have you chosen that strategy?

- How will this adapt over time?

Good retirement planning should include:

- Cashflow modelling (as a guide, not a prediction)

- Regular reviews

- Adjustments as life and markets change

Across the firms I work with, a key focus has been building consistency in how retirement is approached — not just for compliance, but for better client outcomes.

Key message: Retirement is actively managed.

In Summary

Saving is about building wealth.

Retirement is about making it last.

They require different thinking, different structures, and a different mindset.

And perhaps the most important takeaway is this:

The hardest part of investing isn’t growing your money — it’s knowing how to use it.

Add comment

Comments