When you see adverts about retirement, it’s hardly surprising that the first question most people ask is:

“Do I have enough?”

It’s a natural place to start.

But working closely with financial advisers, I’ve come to believe there is a better starting point—one that doesn’t begin with a number, but with you.

Your life.

Your goals.

Your version of retirement.

This approach may not grab headlines in the same way as “you need £1 million to retire”, but it is far more valuable.

Because until you understand what retirement looks like for you, the number itself is just a guess.

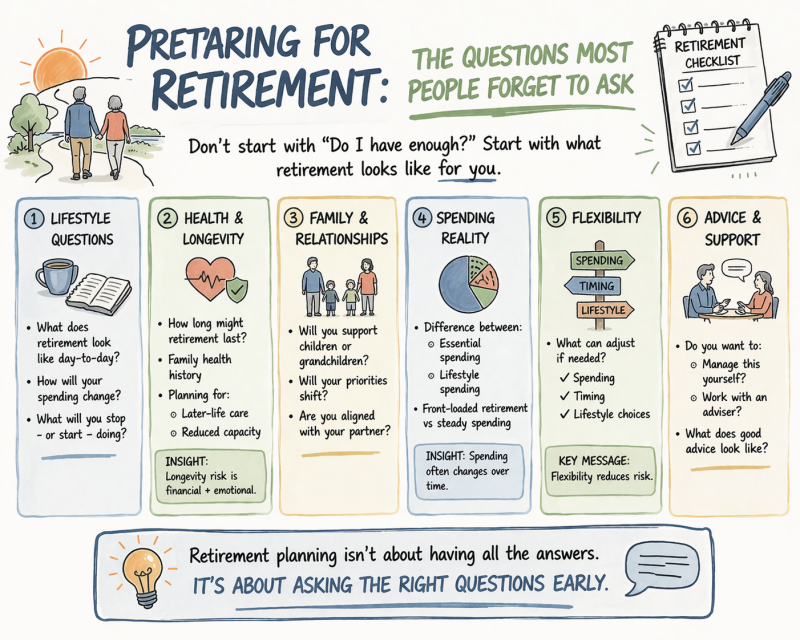

A Different Starting Point

Before focusing on how much you need, it’s worth asking better questions.

You can use the checklist below:

- On your own

- With your partner

- Or as a starting point with a financial adviser

Lifestyle Questions

- What does retirement look like day-to-day?

- How will your routine change?

- What will you stop doing—and what will you start?

This is where retirement becomes real. Not a concept, but a lifestyle.

Health & Longevity

- How long might your retirement last?

- What does your family health history suggest?

- Have you considered:

- Later-life care?

- Reduced physical or mental capacity?

Insight: Longevity risk is not just financial—it is emotional.

Planning for a longer life requires flexibility, not just funding.

Family & Relationships

- Will you support children or grandchildren financially?

- Will your priorities shift over time?

- Are you and your partner aligned in your expectations?

Many financial plans fail not because of investments—but because of misaligned expectations.

Spending Reality

- What are your essential costs?

- What are your lifestyle costs?

- Will your spending be:

- Higher in early retirement?

- Or more stable over time?

Behavioural insight: Spending is not static. It often changes throughout retirement—typically higher early on, then gradually reducing.

Flexibility

- What can you adjust if needed?

- Spending

- Timing of retirement

- Lifestyle choices

Key message: Flexibility reduces risk.

The more adaptable your plan, the less pressure there is on any single outcome.

Advice & Support

- Do you want to:

- Manage this yourself?

- Work with a financial adviser?

- If you do work with an adviser, what does “good advice” look like to you?

- Clarity?

- Ongoing support?

- Someone to challenge your thinking?

There is no single right approach—but understanding what you need from support is key.

In Summary

Retirement planning is not about having all the answers.

It’s about asking the right questions—early enough to make a difference.

If you take the time to work through these questions, something interesting happens:

You begin to understand what retirement actually looks like for you.

And only then does the question:

“Do I have enough?”

start to become meaningful.

Final Thought

Write this down. Talk it through. Challenge it.

Because the goal is not to start with what you have.

It is to start with:

What retirement is for you.

The numbers will follow.

Add comment

Comments