There is a lot of debate around retirement income and how it should be approached.

For me, the starting point is always the same:

the foundation matters more than the solution.

It is very easy to jump straight into how to take income, but that skips an important step.

What does retirement actually look like?

What is the journey we are trying to support?

Only then can you begin to think about the structure.

Two Common Approaches

If we strip this right back, there are broadly two camps:

- Selling units to provide income

- Living off natural income (dividends/interest)

To illustrate the difference, let’s use a very simple scenario:

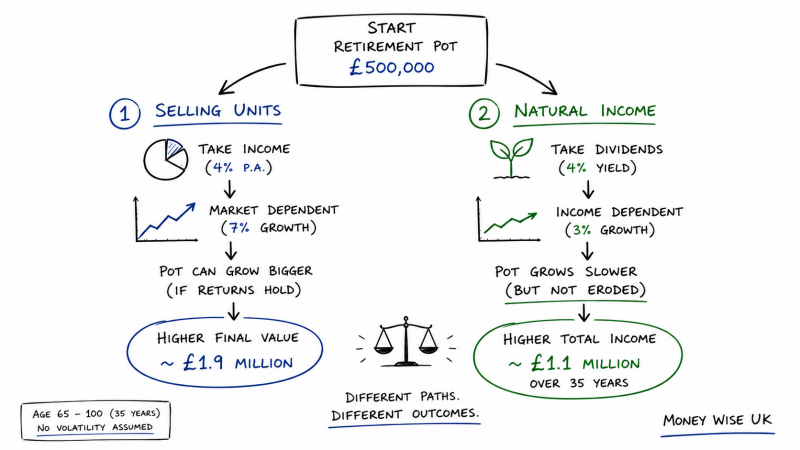

- Starting pot: £500,000

- Time horizon: age 65 to 100 (35 years)

- Withdrawal: £20,000 per year (4%)

- No allowance for market volatility (important caveat)

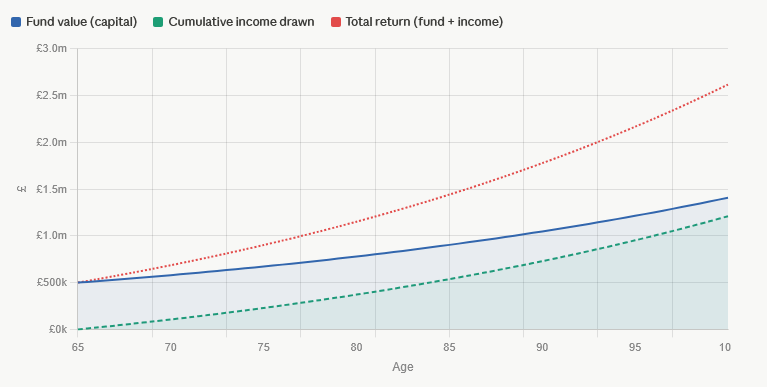

Strategy 1 — Selling Units

(7% growth, 4% withdrawal)

In this scenario, the portfolio grows at 7% per year while supporting withdrawals of £20,000.

What happens?

- The growth rate comfortably exceeds the withdrawals

- The fund not only sustains itself — it grows over time

- By age 100, the portfolio reaches c. £1.9 million

- Total income taken: £700,000

- Total combined value (income + fund): £2.6 million+

On paper, this looks compelling.

But it relies on something important:

returns arriving in the right order.

This is where sequence of returns risk comes in — poor returns early in retirement can significantly change this outcome.

Strategy 2 — Natural Income

(3% growth, 4% yield)

Here, the focus is different.

Instead of selling assets, you are living off the income the portfolio naturally produces.

What happens?

- Capital grows more slowly at 3%

- The portfolio is not eroded — no units are sold

- Income rises over time as the fund grows

- By age 100, the portfolio reaches c. £1.45 million

- Total income received: c. £1.1 million

The outcome is structured differently:

- More income over time

- Less terminal capital

The Real Trade-Off

This is where it gets interesting.

- Selling units

- Higher potential growth

- Greater reliance on market conditions

- Exposure to sequencing risk

- More flexibility in how income is taken

- Natural income

- More stable and intuitive approach

- Less reliance on timing

- Income linked to underlying assets

- Typically lower overall growth

Neither is “right”.

They are simply different ways of solving the same problem.

What Really Matters

The mistake is trying to find the answer.

The better question is:

what outcome are we trying to achieve?

- Is it stability of income?

- Is it maximising long-term wealth?

- Is it avoiding selling investments during market falls?

- Is it leaving a legacy?

Because once you understand that, the structure becomes clearer.

The Behavioural Shift

The biggest change in retirement is not financial — it is behavioural.

You move from:

- Accumulating wealth

to - Relying on it

That shift brings uncertainty.

And this is where good planning matters more than the specific strategy.

Final Thought

Both approaches can work.

Both can fail.

And both are highly sensitive to factors we haven’t modelled here —

particularly market volatility, inflation, and longevity.

The right solution is rarely one or the other.

More often, it is a blend.

A structure that provides:

- Income stability in the short term

- Growth to support the long term

- Flexibility to adapt along the way

Because retirement isn’t a single decision.

It is a journey that needs to be managed over time.

Add comment

Comments