I recently spoke to Emma Mogford at Premier Miton on the Money Wise UK podcast. We were discussing risk, and I asked a fairly extreme question: what happens to retirement income if markets drop by 50%?

The answer shouldn’t surprise anyone. But the implications might.

Client A: selling units to fund retirement

Take a client with a £100,000 pot withdrawing £5,000 a year — 5% of the fund. If markets fall 50%, the pot drops to £50,000. If they continue drawing 5%, income drops to £2,500.

If they try to maintain £5,000, they sell twice as many units into a falling market. That accelerates the depletion of the pot.

Either way, the income is not sustainable at the original level. The fund and the income are inseparable. This is sequencing risk in its most visible form.

Client B: living off dividends

Dividend income works differently. Income is paid per share — so it is the number of shares that matters, not the market price. If markets fall and the portfolio drops in value, Client B still holds the same shares. The income continues unless the company cuts its dividend.

I have seen this play out in my own portfolio. Some of my investment trust holdings have fallen around 30% in value — yet I am still receiving dividend income of over 10%. The capital value dropped. The income did not.

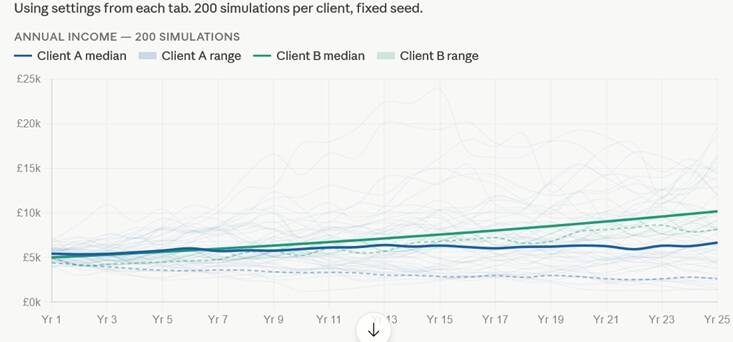

What the modelling shows

I ran both scenarios through a Monte Carlo simulation — 200 simulations over a 25-year retirement period. The chart below shows the range of possible income journeys for each client.

The results are striking.

If Client A adjusts their withdrawal to always reflect 5% of the current fund value, income can range anywhere from £2,525 to £14,815 (best and worst 10% all years). Markets go up, income goes up. Markets fall, income falls. The variability is baked in by design.

Client B starts at £5,000 and — based on a modest assumption of dividend growth — reaches around £10,164 by year 25 in the median scenario. The income variation is between £4,120 and £10,164 (best and worst 10% all years). The income band is tight. It drifts upward. The occasional dividend cut creates a temporary dip, but the trajectory is clear.

So which approach is right?

Neither — and both.

Client A has real merit. If the investment strategy delivers strong long-term growth, the fund has the potential to grow significantly. Income variability is the trade-off for that upside.

Client B has real merit too. The units remain intact. The income journey is smoother. The main risk is dividend cuts — which happen, but are typically partial and temporary.

The problem is not the strategy. The problem is when the client does not understand the journey they are on.

One practical point worth noting for Client B: dividends are often paid at different stages — monthly, quarterly, or irregularly. Finding a way to smooth that income is an important planning decision in its own right.

The real question to ask

Like the active vs passive debate, you can blend both approaches. A portfolio combining natural income with capital growth is not a compromise — it can be a deliberate and well-constructed strategy.

But it has to start in the right place.

Not with what the financial planning firm is comfortable recommending. With what journey the client is comfortable being on.

Retirement income sustainability is not just a technical question. It is a behavioural one. The best strategy is the one your client can stick to when markets fall 30% and their statement makes for uncomfortable reading.

Understand the journey first. Build the strategy around it.

Was this worth a coffee? Not a flat white. Just a regular, sensible £2 coffee. If this helped, feel free to buy me one. If it didn't, keep your money — that's only fair.

Add comment

Comments