One of the things I learned in the 1990s was the power of understanding returns.

Back then, insurance company funds were effectively the closest thing we had to trackers. For most people with endowments and PEPs, that was it. If you wanted to go further, you could buy unit trusts — but your research was largely limited to a performance table in the back of a newspaper.

Towards the end of the decade, something shifted. As those tracker-like funds slowed, I started to notice that certain other funds were outperforming by a meaningful margin. That caught my attention.

Then came three consecutive years of negative market returns. And that's when something important became clear — active managers who knew what they were doing could deliver better outcomes than the market, even when the market was falling. Not always positive returns. But better. And in a falling market, better is everything.

That, perhaps, is the point.

Blinkered by what we know

From around 2009, markets delivered what felt familiar to me — double-digit returns, strong momentum, the wind behind passive investing. Different environment to the 90s in many ways, but the return profile felt recognisable.

The problem? My frame of reference was the 90s. That shaped how I thought. And it made me wonder — how many investors today only know markets from 2009? How many advisers have built their entire investment philosophy in a period of almost uninterrupted market growth?

That's a blinkered view. And blinkered views tend to get exposed.

Active vs passive is the wrong debate

Today, the passive versus active debate dominates. But whichever side of the fence you sit on, I think the more important question is this: do you actually understand what you own?

Active investing now covers a wide spectrum. At one end, you have pure index-tracking. At the other, a manager making genuine decisions about what to hold and why. In between, there's factor tilting, smart beta, blended approaches. The debate often centres on cost — 0.05% versus 0.85% — but remember, the performance figures you see already account for those charges. So you can quickly judge whether the cost is worth paying.

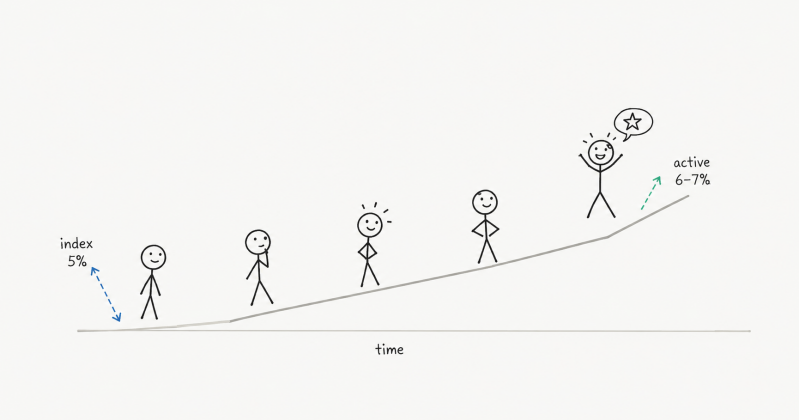

I've produced the chart below to show how even a small difference in returns — sustained over time — can make a very significant difference to the outcome.

What the chart also shows is that this isn't straightforward. A fund averaging 1% above the index won't beat it every single year. There will be periods where it lags. But compounded over ten, twenty, thirty years, the gap becomes hard to ignore.

What I did — and what it taught me

When I managed portfolios, I took the time to understand the funds I was investing in. I looked at whether the opportunity was genuinely there. I considered the market environment. Sometimes that meant blending styles rather than backing one approach entirely.

Over ten years, I delivered returns significantly above the index.

Could I do it today? Honestly, it's difficult to say — I stopped managing portfolios two years ago. But the principle holds. Do the work. Understand what you own. Be willing to adapt.

The challenge — for investors and advisers alike — is what happens when passive just delivers the market and the market is poor. Because it will happen. It always does at some point.

It was never about right or wrong

This debate should never be framed as passive good, active bad — or the other way around. It's about understanding what you hold, why you hold it, and what it might reasonably return in the environment ahead.

That's the power of understanding. And it's something no algorithm can replace.

The chart above is for illustrative purposes only. All returns shown are net of charges. Past performance is not a guide to future returns. Investments can fall as well as rise in value.

Was this worth a coffee? Not a flat white. Just a regular, sensible £2 coffee. If this helped, feel free to buy me one. If it didn't, keep your money — that's only fair.

Add comment

Comments