I’m borrowing that headline to make a point.

A few years ago, I came across an article built around those three statements. Each one was supported by data. Each one was true. But taken in isolation, each told a completely different story.

That has stayed with me.

Because it feels very relevant when looking at the recent headlines around the FCA’s advice review.

You may have seen some of them:

- “FCA to drop annual suitability requirement in landmark proposals”

- “FCA: We want advice firms to offer new fee structures”

- “FCA consultation removing the requirement for annual reviews”

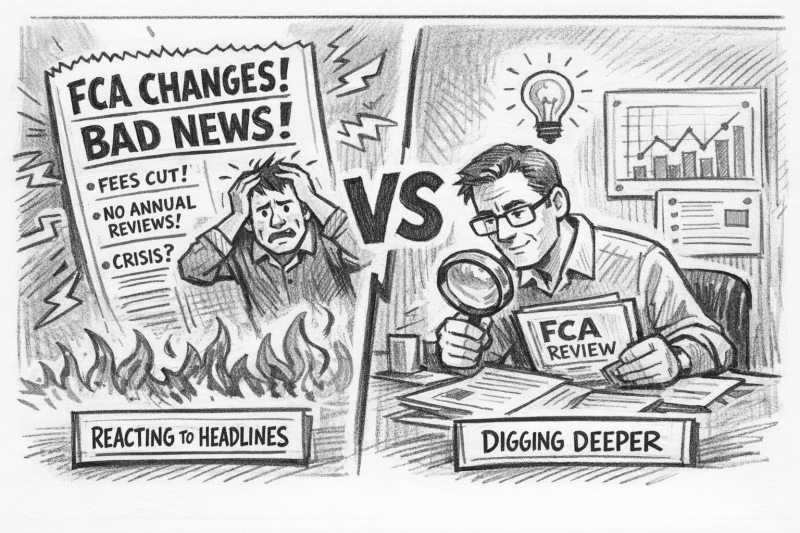

If you stopped there, you could be forgiven for thinking this is all bad news.

And, to be fair, many advisers seem to be reacting that way.

Spend a few minutes on LinkedIn and you’ll see it:

- “This is bad for business”

- “We’ll be forced to cut fees”

- “Suitability reports won’t be needed”

- “Annual reviews are disappearing”

But this is where the earlier point matters.

Headlines are not the full picture.

You have to dig deeper

I remember a conversation with a fund manager about China. His view was simple: if you only read Western headlines, you would struggle to find anything positive. But that doesn’t mean the opportunity isn’t there.

You just have to look beyond the surface.

The same applies here.

When you take the time to read the FCA papers in full, a different picture begins to emerge.

Not one of deregulation or dilution.

But one of flexibility, clarity, and—importantly—opportunity.

A shift towards proportionate advice

One of the most significant changes is the move towards allowing more proportionate, targeted, and simplified advice.

For firms already offering one-off or transactional advice, this could be transformative.

It removes friction.

It provides clarity.

It legitimises models that already exist but have often operated in grey areas.

And when you bring this into the context of retirement planning—where needs change, decisions are staged, and not every client requires a full ongoing service—it starts to feel particularly relevant.

Not every client needs the same level of intervention at the same frequency.

And deep down, most advisers already know that.

Annual reviews: requirement vs reality

There has been a lot of noise around the potential removal of a strict annual suitability requirement.

But the real question isn’t:

“Do we have to do annual reviews?”

It’s:

“What does good ongoing service actually look like for this client?”

For some clients, that may still mean structured annual (or more frequent) reviews.

For others, it may be different.

The direction of travel is towards justifying the service based on client need, rather than defaulting to a fixed model for everyone.

That is a subtle but important shift.

The real challenge: demonstrating value

If there is a genuine challenge within all of this, it sits here.

Not in fees being “cut” or reviews being “removed”.

But in clearly demonstrating:

- What clients pay

- What they receive

- And, crucially, the outcomes delivered

It still surprises me how few firms openly display their fees.

Even fewer clearly articulate what those fees cover.

For one of the firms I work with, we’ve taken a different approach:

- Full fee transparency on the website

- A clear statement of what the ongoing fee delivers

- Structured reporting across areas such as vulnerability, decumulation risk, and service delivery

When you read the FCA papers, this is exactly where the emphasis is heading.

Not less accountability.

More.

But in a way that is aligned to outcomes, not just process.

Evolution, not revolution

For many of the firms I work with, these changes are not a fundamental overhaul.

They are a refinement.

A continuation of a direction already being travelled:

- Better articulation of value

- Clearer client segmentation

- More thoughtful service design

- Stronger MI and governance

Yes, there will be work to do.

But for firms already focused on good client outcomes, this feels more like a tweak than a transformation.

A choice of perspective

Which brings me back to where we started.

The world is awful.

The world is much better.

The world can be much better.

All three can be true.

The same applies here.

You can view these changes as a threat.

Or you can view them as an opportunity to:

- refine your proposition

- better align services to client needs

- and clearly demonstrate the value you already deliver

As always, the answer is unlikely to sit in the headline.

It sits in the detail.

Final thought

I don’t claim to have this perfectly right.

And I would welcome challenge—because that is how we improve as a profession.

But if there is one takeaway, it is this:

Be careful not to outsource your thinking to headlines.

Take the time to read.

To reflect.

To discuss.

Because the firms that do will likely be the ones that benefit most from what comes next.

Add comment

Comments